Zerohedge

...just ask Canadians, half of whom said in response to a new Ipsos Reid survey that they are within $200 per month of not being able to pay their bills and make their debt payments.

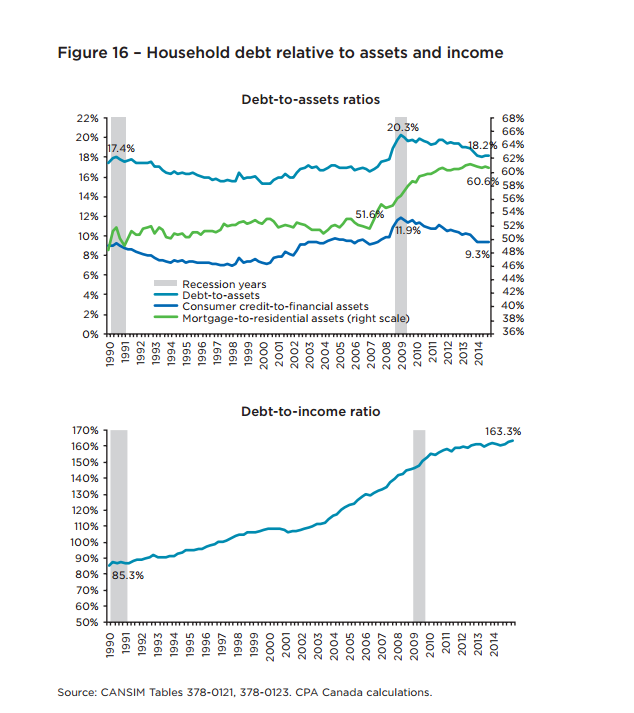

"Ipsos Reid conducted the poll about a week after the Parliamentary Budget Office issued a report on Jan. 19 that said Canada has seen the largest increase in household debt relative to income of any G7 country since 2000," The Calgary Herald writes, adding that "31 per cent of respondents said any increase in interest rates could move them towards bankruptcy".

The survey also found that 25% of Canadians are already unable to cover their bills and service their debt.

Bloomberg

Demand for new condominiums in Canada’s oil patch sank the most last year since 2008, according to data from Altus Group Ltd. Sales of condos in Calgary fell 38 percent to about 3,000 units from 4,805 units the prior year, according to the Toronto-based real estate consulting and advisory firm. That’s the biggest year-over-year drop since the financial crisis in 2008, when transactions fell 72 percent to 1,103 units.

...just ask Canadians, half of whom said in response to a new Ipsos Reid survey that they are within $200 per month of not being able to pay their bills and make their debt payments.

"Ipsos Reid conducted the poll about a week after the Parliamentary Budget Office issued a report on Jan. 19 that said Canada has seen the largest increase in household debt relative to income of any G7 country since 2000," The Calgary Herald writes, adding that "31 per cent of respondents said any increase in interest rates could move them towards bankruptcy".

The survey also found that 25% of Canadians are already unable to cover their bills and service their debt.

Bloomberg

Demand for new condominiums in Canada’s oil patch sank the most last year since 2008, according to data from Altus Group Ltd. Sales of condos in Calgary fell 38 percent to about 3,000 units from 4,805 units the prior year, according to the Toronto-based real estate consulting and advisory firm. That’s the biggest year-over-year drop since the financial crisis in 2008, when transactions fell 72 percent to 1,103 units.

RSS Feed

RSS Feed